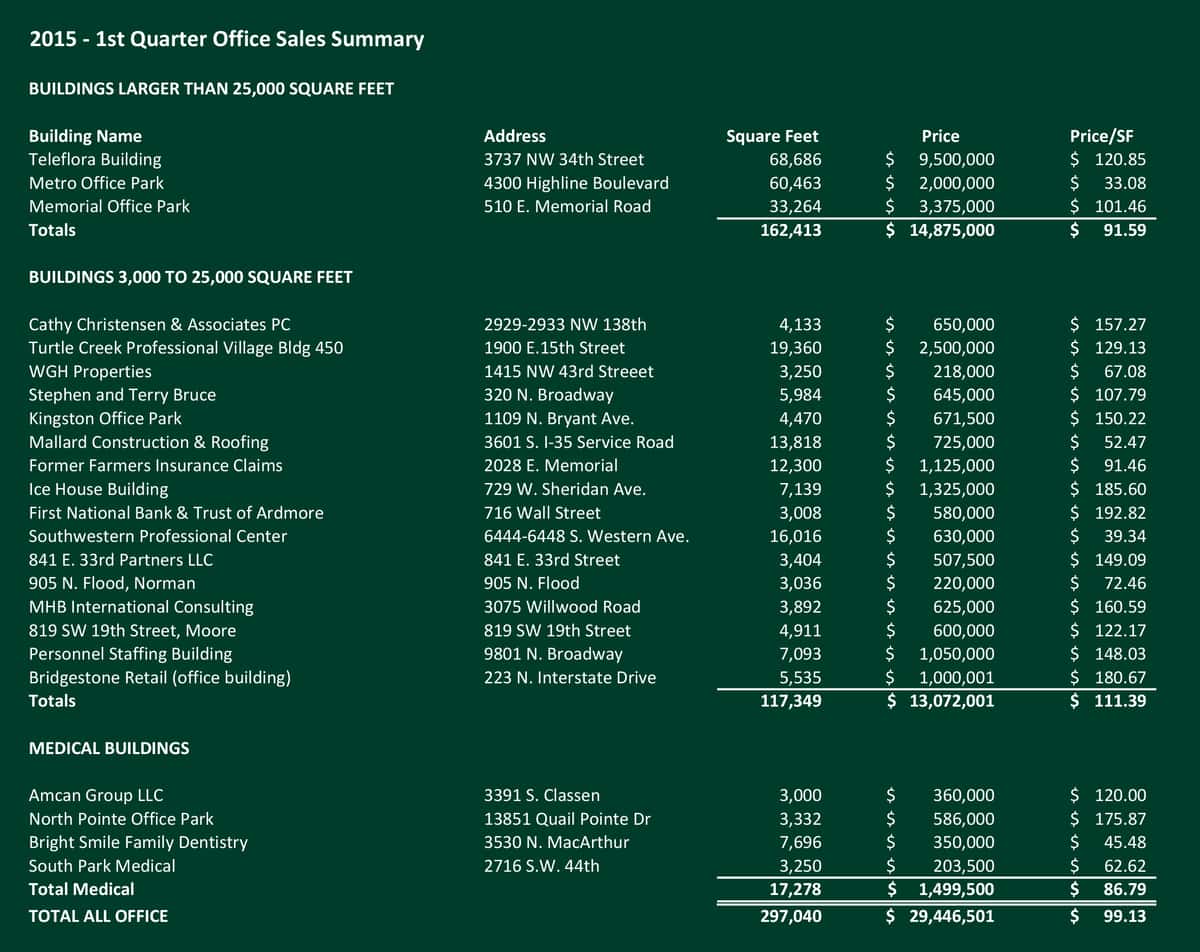

Office Market Healthy with over $29 Million in First Quarter Sales

Office sales for the 1st Quarter of 2015 continue to show a healthy market for office buildings in Oklahoma City. A total of $29,446,501 in office properties containing 297,040 square feet changed hands during the quarter. Average price for all buildings was $99.13 per square foot. Three buildings in excess of 25,000 square feet accounted for 162,413 square feet at an average price of $86.32 per square foot. Two of the buyers were local and one was an out of state group. Nineteen buildings of less than 25,000 square feet made up the balance of the sales. The 19 smaller buildings accounted for 117,349 square feet at an average on $111.39 per square foot. The highest price per square foot paid for any building was on Film Row in the CBD.

As one examines the market and studies the atmosphere of office investors it becomes clear that there is a significant amount of money in search of investment opportunities. Over the years Oklahoma City has positioned itself well with continued growth in the health sciences, petroleum, R & D and Tinker Air Force Base. We are bolstered by a healthy economy, still low unemployment and an enthusiastic citizenry. These attributes, along with a rebounding oil and gas sector, should prove to be a combination that will continue to move us forward.

Retail Investment Sales Slow

Retail investment sales slowed during the first quarter of 2015 after hitting a seven-year high in 2014. Three sales occurred during the first quarter totaling 222,297 square feet for a total of $6.65 million in value. The two larger centers were older with some deferred maintenance located in mature areas; the sale price of the two averaged $19.07 per square foot. The third sale was a newer strip center at the Oklahoma City/Edmond border that came in at $137 per square foot.

One quarter and three sales are probably too limited of sample to read much into; however, the trend we’ve seen the last few years of sales on the lower end and sales on the higher end appears to continue. There are a couple of Class A projects being marketed for sale and could possibly close in the second quarter, Belle Isle Station chief among these. Given the limited availability of this type of project and continuing interest in our market from multiple out-of-state institutional investors, we expect capitalization rates on these deals to be very low. The anxiety locally about energy prices does not yet appear to be affecting these investors. And, while we do not expect to reach last years sales levels, we do see a pick up in volume over the course of the year.

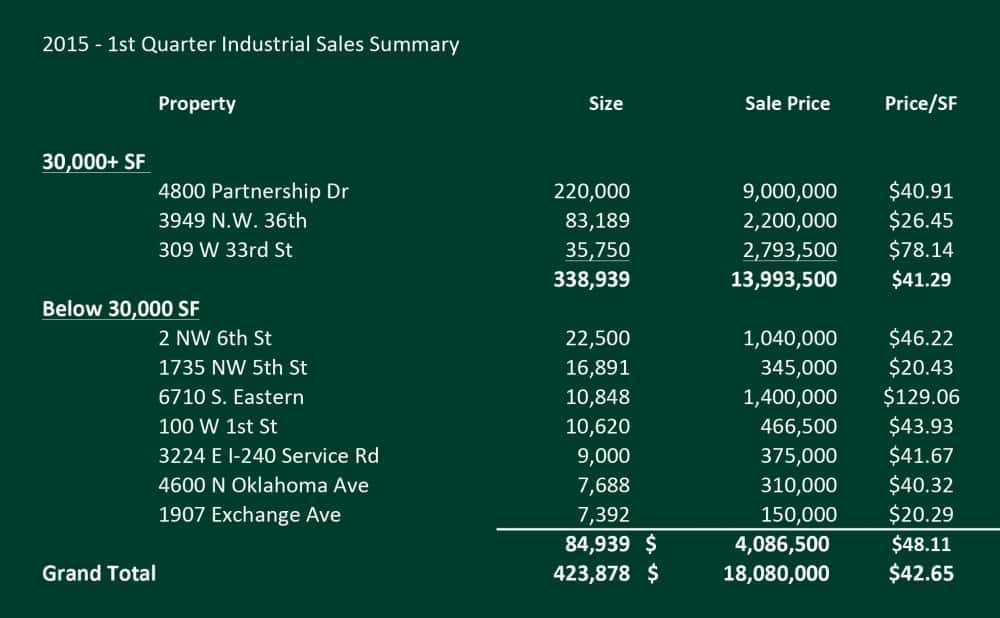

Vacancy Critically Low in Industrial Market

After a landmark year of industrial sales in 2014, 2015 has started quietly. This is, without a doubt, a consequence of the current critically-low vacancy rate in the industrial market, in the range of 5.75%-6%. Although low vacancy is the sign of a vibrant market, when the vacancy rate gets too low it translates to a lack of available alternatives available for expansions or new-to-market firms, resulting in stagnation. Overall there were 10 industrial buildings sold containing 423,878 square feet for a total consideration of $18 million. Two of these were investor purchases over 30,000 square feet, the largest being an 83,189 square foot building in the former Little Giant Pump complex. The largest sale was 220,000 square feet of bulk warehouse space to a local grocery retailer. The overall average price per square foot was $42.65. The 1st quarter of 2014 saw 16 sales totaling 821,775 square feet for $21.8 million.

The drop in the price of oil has and will continue to affect the industrial real estate market. However, the low vacancies are more related to the overall economy than one particular sector. We do not expect any radical changes in occupancy in the industrial market in the foreseeable future.

Average Price on Class B and C May Rise in 2015

In the first quarter of 2015, the Oklahoma City multifamily market had a total of six transactions totaling 1,024 units for a sales volume of $44,830,758. This is an average price per unit of $43,780, with all but one transactions being Class C, and the other property sold a B Class asset. The average price per unit for Class C transactions was $37,767. With a volume of $29,080,750 representing 770 units, this average represents the highest per unit average paid for C Class properties in the Oklahoma City market. One Class B property traded hands in the first quarter for $15,750,008 totaling 254 units accounting for $62,007 per unit.

While Class C properties are reaching new heights, the total sales volume was down 44% from the 1st quarter of 2014, and 49% from the previous quarter. Although the volume was significantly down, average price per unit across all transactions increased 16% compared to the same quarter in 2014 and was only slightly down 3% from the previous quarter, although when removing the A-Class transactions was up 7% from the previous quarter. This is a very clear indicator that the market is surging to new levels, and demand is at an all-time high.

In recent history, Class A transactions have dominated the headlines; however, going forward expect to see the influx of capital from out of state investors pushing the average prices up on both B and C Class assets throughout 2015 and even into 2016. For owners who have waited on the sidelines looking for a good opportunity to sell, now appears to be that time.