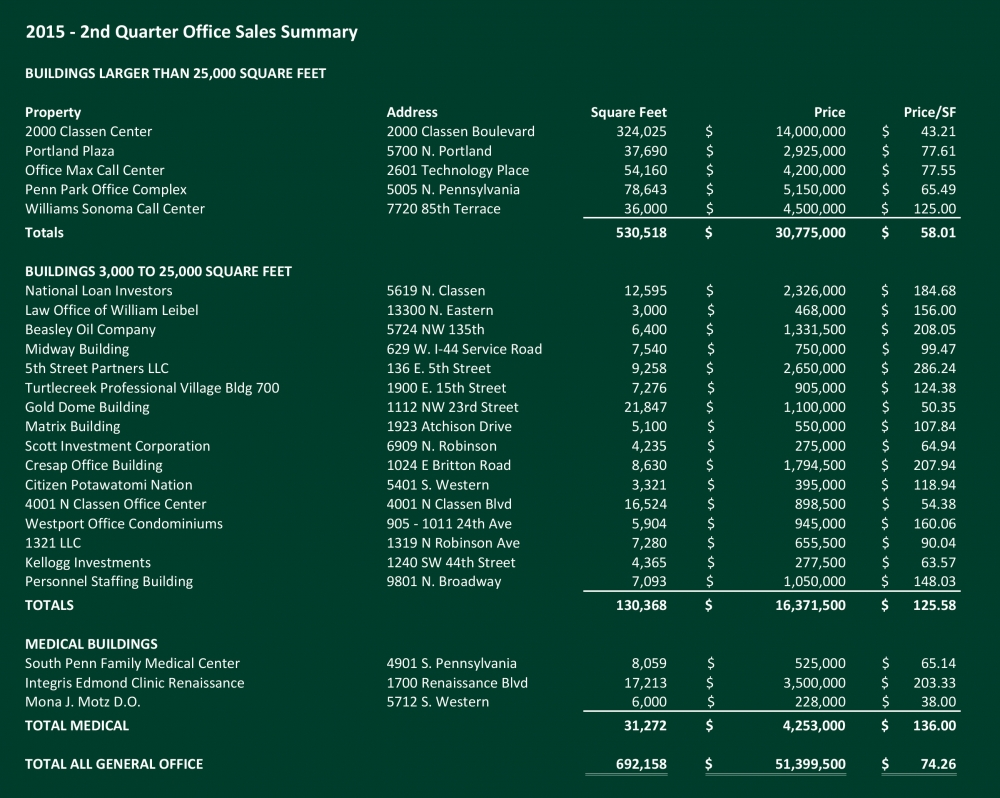

Office Market Exceeds $51 Million in Second Quarter Sales

The 2nd Quarter of 2015 saw 24 buildings change hands in the Oklahoma City office market. This number compared favorably to 20 buildings in the 1st Quarter. Total square footage for the 2nd Quarter was 692,158 square feet at an average of $74.26 per square foot for a total volume of $51,399,500. The most notable sale was the 2000 Classen Center project. The three building complex contains a total of 324,025 square feet and sold to local investors for $14,000,000, or $43.21 per square foot. The complex was the Headquarters of American Fidelity Insurance Company which is moving to the former OPUBCO building at 9000 Broadway Extension.

Five buildings in excess of 25,000 square feet containing a total 530,518 square feet sold for an average of $58.01 per square foot. A total of 16 buildings in the range of 3,000 to 24,999 square feet sold for an average of $132.98 per square foot. The disparity in price per square foot between the larger buildings and the smaller ones is evidence of the continuing demand for small office buildings and the newer vintage of many of the small buildings.

None of the information reviewed reflected any indication of the expected, but as yet unseen, fallout from the price decline in oil having a negative effect on the office market. The potential sale of the Sandridge Energy Campus and the pending sale of First National Center are the major question marks in the Central Business District.

Belle Isle Station Leads Second Quarter Retail Sales

The 2nd Quarter sale that stands out is Belle Isle Station; this 15-year-old power center traded at a 5.4 percent capitalization rate. This is fully 125 basis points lower than any other power center sale in the last 5 years, which translates into almost $10 million in additional value. While the location of the center next to Penn Square Mall and its Nordstrom Rack anchor account for some of the value, much can be traced to aggressive national firms with lots of money to place and a lack of investment alternatives for this type of retail asset. This acquisition is the fourth class A retail property Kite Realty has purchased in the OKC market.

It’s hard to read too much into one sale. But we have been a seller’s market for a number of years with far more potential buyers than sellers. It remains to be seen if the Belle Isle sale is a signal that capitalization rates are headed down for all classes of product. Perhaps this will entice a few more sellers to enter the market.

Inland, now InvenTrust Properties, sold the Village at Quail Springs, anchored by Gordmans to another national REIT. InvenTrust has been getting some pressure from shareholders to sell some properties in an effort to maximize returns; this sale appears to be part of that response. The remaining sales were indicative of our non-class A sales over the past several years, that is, sales are split between larger distressed properties sold at a discount or smaller strip center sales.

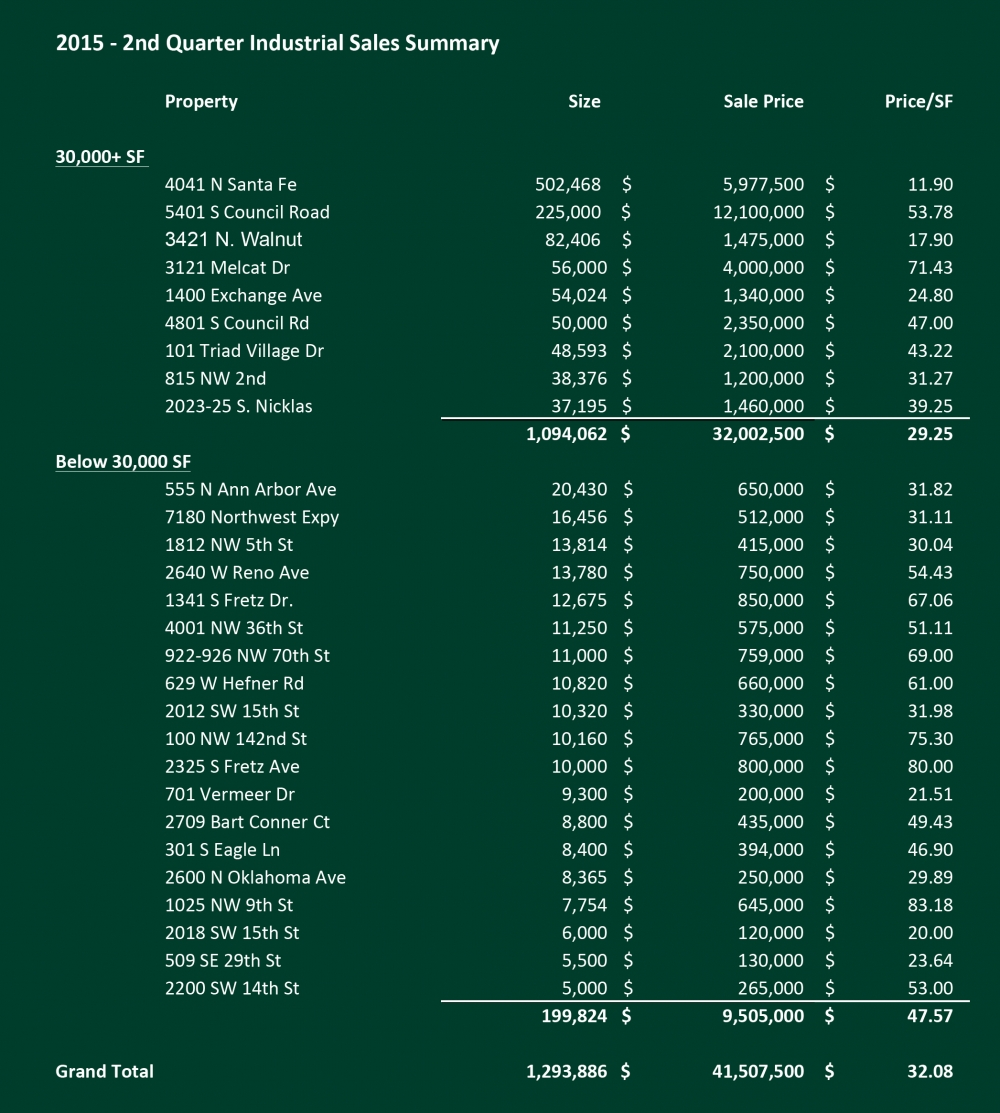

Industrial Sales Rebound in Second Quarter

From a very quiet 1st quarter, industrial building sales have rebounded in the 2nd Quarter of 2015. The list is mixed and includes several older facilities purchased by re-developers. This signals a confidence in the OKC industrial market that transcends the currently depressed crude oil pricing. Overall there were 28 industrial buildings sold containing 1,293,866 square feet for a total consideration of $41.5 million. Two of the purchases over 30,000 square feet fall into the re-development category. The largest overall sale was a portfolio sale-leaseback of the Macklanburg-Duncan manufacturing campus comprising 502,468 square feet of manufacturing and corporate office space to a private equity fund. The market-wide average price per square foot in the 2nd quarter was $32.08, heavily skewed by the relatively low price of the Macklanburg-Duncan transaction.

All things considered in an economically chaotic world, the Oklahoma City industrial real estate market is doing well. During 2014 the total market vacancy rate declined steadily from 6.8% to 5.8% at year-end. During both quarters of the present year, the vacancy rate has remained level at 6.2%. These low availabilities will continue to support the growth we have seen in rental rates, although leasing velocity lacks last year’s momentum.

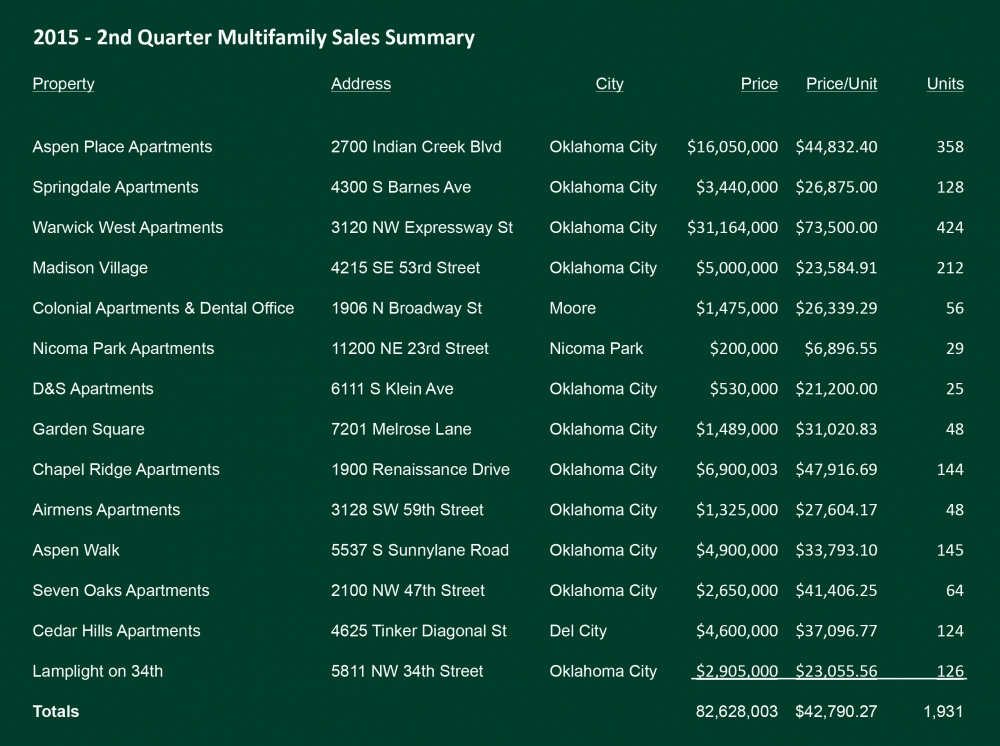

Multifamily Sees an Active Second Quarter in 2015

In the second quarter of 2015, the Oklahoma City multifamily market was very active with a total of 14 transactions totaling 1,931 units for a sales volume of $82,628,003. This is an average price per unit of $42,790, with 12 of the 14 transactions being Class C, one Class B, and one Class D. The total sales volume was up 81% with $45 million in transaction volume in the previous quarter. This brings a total 2015 sales volume for all multifamily properties to $128,287,261, 28% higher than the same period of 2014.

Class C properties were the most active with 2,632 units trading so far in 2015, with no Class A transactions, compared to the first half of 2014 which had two Class A transactions totaling $52 million. There were two B Class transactions in 2015, one in the first quarter and the second in the second quarter totaling $22,650,011. The average price per unit increased by 25% to $56,910 compared to the previous year’s first half. This increase was partly due to the previous year including a portfolio transaction with an average price per unit below what most considered market value. The only Class D transaction for the year was in the second quarter which had an average price per unit of $6,897; there were none in the first half of 2014.

Overall, the data indicates that with the lack of distressed properties, and the soaring average prices per unit paid, the market is very robust and stabilized properties are in demand. The most active buyers are regional and national value-add investors picking up stabilized Class C assets looking to increase the investment yield from implementing upgrades and management changes. This is very similar the mid- 2000’s; however, the buyers of today are slightly more conservative with their projections. The lack of Class A transactions is not for a lack of buyers, rather it’s a lack of inventory. We expect to see some transactions over the next twelve to eighteen months as a few new projects near completion and are brought to market. For now, all eyes are on interest rates to determine how long this market expansion will last. So far, most transactions are based on values using current income, so when interest rates increase there shouldn’t be a decline in values, but more of a stabilization. Should values continue to increase at the pace they’ve increased over the last two to three years, there will be more room for concern. For now, we remain bullish about the near future while keeping a close eye on how quickly interest rates increase once they do begin to move upward.