Oklahoma City’s retail market continues to defy easy explanations.

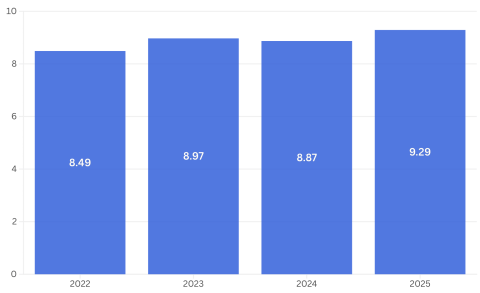

On the surface, the numbers suggest stability. The metro closed 2025 with a retail vacancy rate of 9.29%, up modestly from 8.87% the year prior, across a total market of 50.4 million square feet. In many parts of the city, demand is steady enough to keep business owners genuinely optimistic.

As Price Edwards & Company broker Rosha Wood noted in the firm’s year-end retail summary, locally owned retailers and restaurants across Oklahoma City experienced moderate sales growth in 2025, even as many continue to face pressure from rising costs, staffing shortages, and e-commerce competition. That balance between stability and strain is defining the market.

A Market That Looks Healthy and Feels Tight

Oklahoma City’s retail fundamentals remain solid by most measures. The market tracks 31.3 million square feet across larger developments and another 19.1 million square feet in stand-alone buildings, with Price Edwards estimating an additional 13.5 million square feet of smaller strip centers under 25,000 square feet.

But overall vacancy nudged up to 9.29% in 2025, and absorption slowed to just 0.06 million square feet, down from 0.28 million the year before. Those numbers are not alarming on their own, but they reflect something important: the market is becoming more selective. Demand is concentrating in higher-quality assets, while secondary and older properties are seeing slower leasing activity and softer rents.

For independent retailers, the practical reality is not whether space exists. It is whether the right kind of space exists at a price that makes sense. A storefront may be technically available, but if build-out costs are too high, concessions are too limited, or the location does not generate consistent traffic, it is not really a workable option. That is why so many local businesses in OKC feel hopeful and squeezed at the same time.

Why Usable Space Matters More Than Available Space

One of the quieter pressures facing local retailers right now is the shortage of truly usable space.

As new retail construction has slowed, businesses are competing for a smaller pool of quality locations. That hits hardest for the kinds of tenants that need visibility, flexibility, and manageable startup costs. Vanilla shell space — the unfinished, configurable units that let a boutique or specialty food concept build around their own operation — has become increasingly scarce. When that inventory shrinks, tenants lose leverage. They absorb more of the upfront build-out cost and receive less landlord contributions to offset it.

That may be manageable for a regional chain with a deep balance sheet. For an independent operator running on thinner margins, it can become a serious barrier to entry.

This is where experienced retail brokers earn their value. In a tighter market, success is not just about finding an open suite. It is about identifying the right submarket, the right neighbors, and lease terms that actually support long-term business health.

Why Neighborhood Centers Are Pulling Ahead

One of the clearest shifts in the Oklahoma City market is the growing strength of unanchored neighborhood and service-oriented retail centers.

These properties are home to the kinds of businesses people cannot fully replace online: coffee shops, salons, fitness studios, local restaurants, boutiques, and other concepts that rely on repeat visits and personal connection. They fit the way people actually live. Customers want convenience, but they also want places that feel local, familiar, and worth coming back to.

That is why walkable districts and neighborhood-focused corridors continue to outperform. Areas with a strong sense of place do more than offer square footage — they create habits.

More and more, local businesses are willing to pay a premium for spaces that offer energy, visibility, and neighboring tenants that strengthen the destination. As Price Edwards Chief Operating Officer Jim Parrack put it in the firm’s year-end report:

“The flight to quality is real in OKC. Well-located, high-performing assets are trading

at prices that would have seemed aggressive just a few years ago.”

— Jim Parrack, COO, Price Edwards & Company

That flight to quality is no longer a passing trend. It is becoming the new baseline.

The Gap Between Strong Centers and Struggling Ones

Not every retail property in Oklahoma City is benefiting equally from that shift, and that divide is one of the most important stories in the market right now.

Some centers are thriving because they align with how people actually shop today — service-driven, experience-focused, conveniently located. Discount concepts continue to thrive given economic uncertainty as well. Others are losing momentum because they depend on older formats, weaker traffic patterns, or tenant mixes that feel increasingly out of step. The gap between those two categories widened in 2025, and there is little reason to expect it to narrow in 2026.

For retailers, that makes location decisions more consequential than ever. A few years ago, a determined operator could make an average space work through persistence alone. Today, if the surrounding businesses are weak, the center lack’s identity, or the area does not generate repeat visits, a business starts at a real disadvantage.

Owners and investors are no longer focused solely on occupancy. Increasingly, they are evaluating whether a shopping center remains relevant to today’s consumers — whether it drives consistent daily traffic, supports service- and necessity-oriented tenants, and aligns with evolving shopping habits and customer expectations.

The Daily Pressure on Independent Retailers

Even when a local business lands in the right location, the operating environment remains demanding.

Food costs are still volatile. Labor is still tight. Overhead is higher. Online competition is always present. And even when consumers are spending, they are more selective about where and what they spend on. That has pushed many independent retailers to get more creative about how they compete.

- Food price volatility → Many local restaurants and retailers are adapting with seasonal menus and partnerships with local suppliers to better manage fluctuating costs.

- Labor shortages → Businesses are operating with leaner staffing models and cross-training employees to improve flexibility and efficiency.

- E-commerce competition → Retailers are leaning into experience-driven concepts such as classes, tastings, events, and custom fittings that encourage in-person visits.

- Rising overhead costs → Some retailers are downsizing their footprints, experimenting with pop-up concepts, or utilizing shared retail spaces to reduce expenses while maintaining market presence.

These are not side strategies. They are part of how local retailers stay competitive in a market that continues to raise the bar.

What Retail Space Needs to Offer in 2026

If Oklahoma City’s independent retail scene is going to stay strong, the real estate has to support it.

That means flexible square footage, practical lease structures, better visibility, and spaces that feel genuinely connected to the neighborhoods around them. It also means property owners need to think beyond simply filling vacancies. The best-performing centers are not just leased up — they are active, useful, and embedded in daily life.

Flexible leasing is becoming a real part of that equation. Pop-ups, shorter-term commitments, and incubator-style arrangements are no longer just stopgaps. In many cases, they are smart tools for bringing energy into a center while giving local operators room to test demand before making a larger commitment. Property owners who once insisted on five-year minimums are discovering that flexibility fills vacancies faster and attracts the kinds of tenants that build long-term community loyalty.

Walkability and placemaking matter too. Corridors with strong pedestrian energy, a clear identity, and neighboring businesses that complement each other consistently outperform those that rely on drive-by traffic alone. That is not a new idea, but it is increasingly the difference between a center that thrives and one that struggles to stay relevant.

Navigating What Comes Next

Oklahoma City’s independent retailers are still showing real resilience. They are adapting, finding creative solutions, and continuing to locate opportunity in a market that has become more selective and more expensive. That resilience matters, and it should not be understated.

But the pressure is real. Good space is harder to secure. Build-out costs are up. The gap between strong locations and struggling ones is getting wider, not narrower. And in that environment, instinct alone is not enough.

What separates the retailers who are simply surviving from the ones who are genuinely thriving is strategic placement, the right lease structure, and the right people helping them read a market that varies significantly from one submarket to the next.

Price Edwards & Company brings decades of OKC retail leasing and property management expertise to owners, tenants, and investors navigating exactly this environment. Whether the focus is evaluating a current tenant mix, identifying new opportunities, or making sense of shifting submarket conditions, their team offers the local insight needed to make confident, long-term decisions. The market still offers real opportunity — for those willing to move strategically.